The latest issue of Music & Copyright is now available for subscribers to download. Here are some of the highlights.

The latest issue of Music & Copyright is now available for subscribers to download. Here are some of the highlights.

SPECIAL FOCUS: Spotify stresses the importance of value as the service begins rolling out a new round of price rises

Spotify has surprised analysts by introducing a second round of price rises in a small number of countries. The move was predicted by the news service Bloomberg in early April and confirmed by the Spotify during the first quarter analyst earnings call. While Spotify offered few details of its future pricing plans, the service did hint that it would be making further changes to its pricing structure and breaking away from the all-in model. This is good news for the recorded-music sector as the growth rates for revenue gains from music subscriptions are slowing down. Moreover, the changes could signal a new way of thinking on price, with future access costs potentially based on more than just the number of account holders.

NEWS FEATURE: Clock ticks on US ban, but uncowed TikTok maintains the music push

TikTok has been making headlines for all the wrong reasons. The Chinese-owned company has appeared almost under siege in the past few months due to legislative efforts to ban it in the US and its licensing disagreement with UMG. The latter situation has now been resolved, and the two companies are back to complimenting each other rather than questioning each other’s business decisions. However, the possibility of prohibition continues to cast a dark shadow. Both situations have obscured TikTok’s efforts to move and shake in the live music business. So far, those efforts look to be paying off, with the company set to become a new force. Some would say that the music industry needs TikTok just as much as TikTok needs the music industry.

SECTOR ANALYSIS: Podcasts play the right music note, but more originality might just pay off

Music-related podcasting has carved out a decent niche with fare that digs deeper into the lives of artists and the ins and outs of writing and producing songs. Podcasting has certainly been appealing enough to attract the participation of major artists such as Dua Lipa and Madonna. However, there’s a sense that production companies aren’t really being adventurous enough when it comes to developing more engaging stories. That’s unfortunate when there is a good chance that more courageous music content might well tempt part of the audience—in particular those superfans—to actually pay for their podcasts.

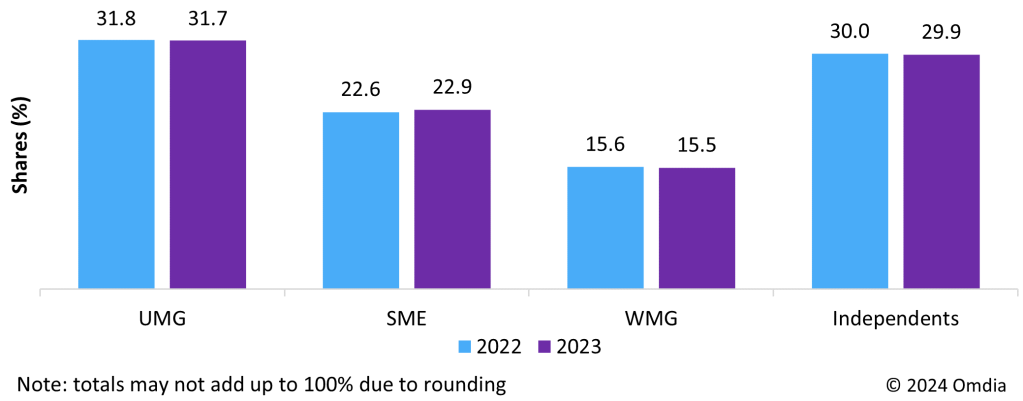

COUNTRY REPORT: Canada

In addition to the usual set of music industry statistics and news briefs, the latest issue of Music & Copyright includes a detailed Canada music industry report. Canada is one of the world’s biggest music markets. Although an ever-present in the top 10, the country has slipped a couple of places in recent years, with the likes of South Korea and China registering higher annual trade sales gains. Recorded-music consumption levels were up in 2023, along with retail sales. Streaming registered healthy growth, with increases in both subscriptions and advertising. Performance rights registered the highest growth rate of the main recorded-music revenue sources. UMG extended its already sizable distributor market share lead despite second-ranked SME’s share rising for the fifth year in a row. SOCAN is yet to publish its full financial results for 2023. However, preliminary figures show that income for the collective management organization topped the prior year’s record high. Canada’s live sector is continuing on the long road to recovery after the impact of the COVID-19 pandemic shuttered the sector for almost 18 months. However, estimates suggest that it will take until next year for ticket sales to return to prepandemic levels.

If you would like more information about the newsletter or to set up a subscription, then send us an email Alternatively, if you would like to download a sample copy, just go here.

Source: Music & Copyright

Source: Music & Copyright Source: Music & Copyright

Source: Music & Copyright Source: Music & Copyright

Source: Music & Copyright The latest issue of Music & Copyright is now available for subscribers to download. Here are some of the highlights.

The latest issue of Music & Copyright is now available for subscribers to download. Here are some of the highlights. The latest issue of Music & Copyright is now available for subscribers to download. Here are some of the highlights.

The latest issue of Music & Copyright is now available for subscribers to download. Here are some of the highlights. The latest issue of Music & Copyright is now available for subscribers to download. Here are some of the highlights.

The latest issue of Music & Copyright is now available for subscribers to download. Here are some of the highlights. The latest issue of Music & Copyright is now available for subscribers to download. Here are some of the highlights.

The latest issue of Music & Copyright is now available for subscribers to download. Here are some of the highlights. The latest issue of Music & Copyright is now available for subscribers to download. Here are some of the highlights.

The latest issue of Music & Copyright is now available for subscribers to download. Here are some of the highlights. The first issue of Music & Copyright for 2024 is now available for subscribers to download. Here are some of the highlights.

The first issue of Music & Copyright for 2024 is now available for subscribers to download. Here are some of the highlights. The final issue of Music & Copyright for 2023 is now available for subscribers to download. Here are some of the highlights.

The final issue of Music & Copyright for 2023 is now available for subscribers to download. Here are some of the highlights.

You must be logged in to post a comment.